The end of ‘install and forget’

For years, residential solar followed a simple logic in the Netherlands: install solar panels, feed excess electricity into the grid and benefit from net metering in the form of near-zero energy bills. However, with the phase-out of net metering starting in 2027, this grace period is coming to an end. Dutch solar owners are now shifting focus toward self-consumption and smart storage to secure further value and savings. Passive generation alone is no longer enough. Almost four million households in the Netherlands already have at least one distributed energy resource (DER). Yet, as uncontrollable photovoltaic (PV) feed-in is further straining the grid, what once was an advantage is now becoming a liability.

The transition away from net metering marks the end of the passive prosumer era in the Netherlands. As PV feed-in becomes less lucrative and grid constraints grow, the focus is shifting toward self-consumption, smarter, money-saving optimization and automation. For households, a battery works as a tool for active optimization, increasing self-consumption and ensuring solar remains an economically sound investment well into the future.

Capturing the Dutch storage boom now

Solar and battery adoption in the Netherlands is moving toward dynamic multi-asset energy management. Around one in three Dutch households already has rooftop PV, making it one of the most mature solar markets in Europe. As net metering is gradually phased out and surplus generation grows, many PV households are now focusing on how they can better use this solar power via storage and smarter system control.

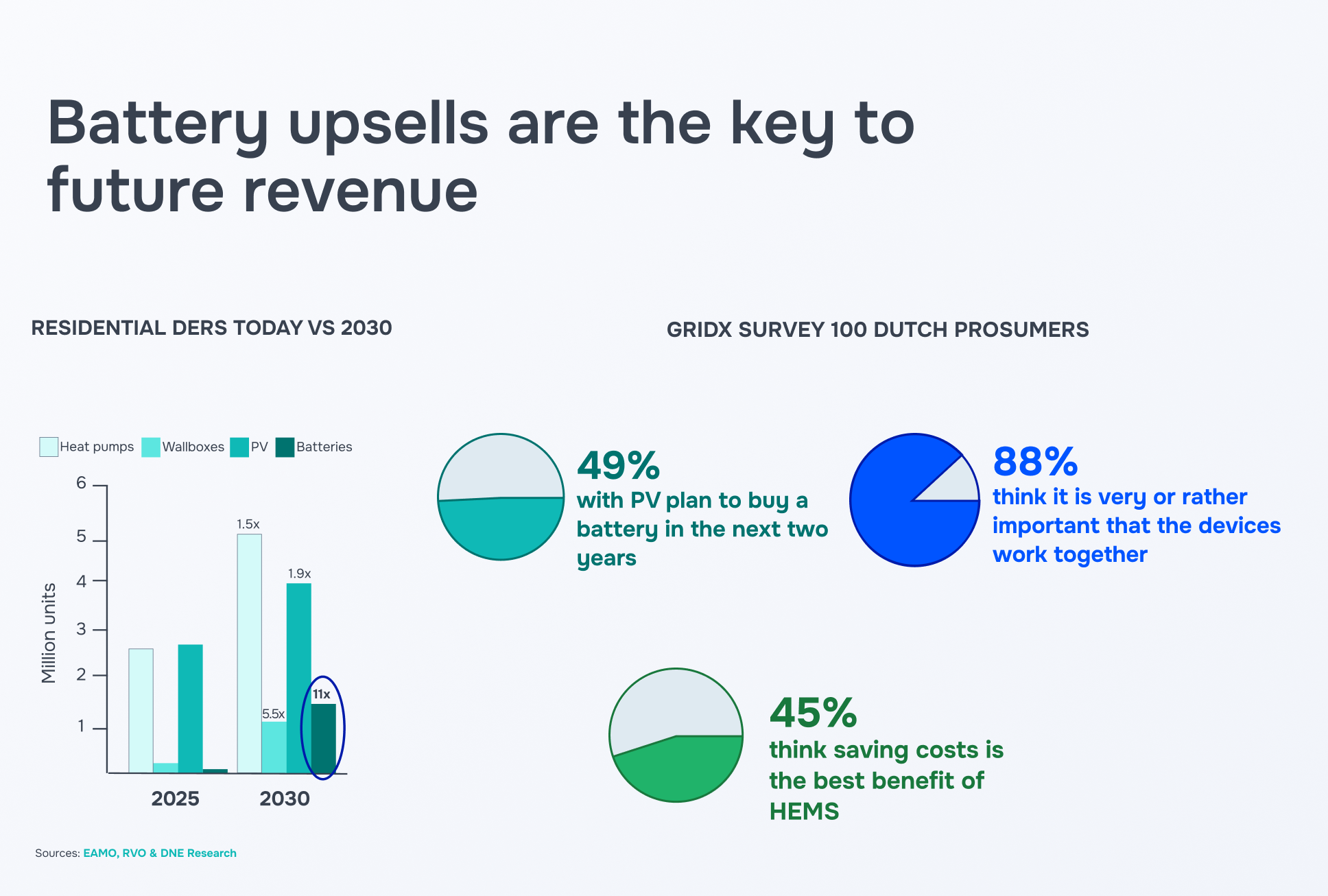

According to gridX survey data, 49% of Dutch PV owners plan to purchase a residential battery within the next two years. Market projections reinforce this direction. Residential battery capacity is expected to scale from roughly 1.3 gigawatt hours (GWh) in 2025 to more than 14.6 GWh by 2030 – a phenomenal 11-fold growth in just five years.

“We are observing a shift where residential energy assets are no longer defined by capacity alone but by their ability to respond to market signals,” comments Irene Guerra Gil, Energy Market Expert at gridX. Integrating solar and battery into an intelligent energy management system that also integrates external signals is what allows households to navigate price volatility and support grid stability.”

Installed hardware alone captures limited value and puts pressure on business margins. As the Dutch market moves beyond pure asset deployment, the real opportunity lies in optimizing connected energy systems to increase revenue per asset over time.

Coordinated flexibility across PV systems, batteries and electric vehicles determines whether households remain passive consumers or actively respond to market and grid signals. Intelligent orchestration turns distributed assets into responsive energy participants that unlock lower electricity costs and new revenue streams.

The competitive advantage from hereon will not lie in the number of installed devices, but in the ability to intelligently control them.

Prosumers want savings

A gridX survey of 100 Dutch prosumers highlights a pragmatic shift in consumer behaviour towards holistic, cost-efficient solutions.

Cost reduction remains the primary driver of new asset purchases, with 45% of respondents identifying savings as the most important benefit of an energy management system (EMS). Furthermore, 88% of prosumers state that it is important that the new hardware works seamlessly with existing systems, reflecting a market that is already saturated with diverse hardware brands. Most consumers remain cautious, with 35% indicating they will only invest in retrofitting once financial savings are clearly proven through real world data.

Turning assets into revenue streams

%201.png)

The economic logic of combining solar and storage is evolving from simple bill reduction to complex value stacking. In the Netherlands, the potential revenue for a household increases significantly as more sophisticated logic is applied. Simple self-consumption optimization provides basic savings of approximately €125 per year, but this increases to €447 per year when time-of-use optimization and dynamic tariff are introduced.

The most significant leap occurs with explicit flexibility. When multiple HEMS use cases are stacked together, including self-consumption optimization, dynamic tariff optimization and participation in wholesale markets through aggregation, annual value can reach up to €1,750 at the very upper end of the spectrum. This figure represents a best-case scenario where solar and battery assets are actively managed across several market layers rather than a baseline expectation. Early implementations in the Netherlands are already testing this approach at scale.

Utilities such as essent have begun enabling smart steering for residential batteries, with hundreds of systems made available for trading within the first months of deployment.

According to Fabian Wolf, Team Lead Customer Success Management at gridX: “What we are seeing in the Netherlands is that value doesn’t come from one single use case. The step from roughly €125 in basic self-consumption savings happens when solar and battery systems combine several optimization layers at once, from dynamic tariffs to flexibility participation. It’s not about pushing households into trading, but about building software that can shift between saving and earning in the background, while self-consumption remains the main priority.”

Flexibility proven at scale

Evidence towards the shift to orchestration is already visible in the Dutch market. A primary example is essent, who has implemented smart steering for residential batteries to manage grid imbalances. This success story demonstrates that the transition from individual self-consumption to system-level orchestration is feasible.

Retailers and aggregators are increasingly steering residential batteries in response to imbalance signals and dynamic pricing, reflecting a broader transition from passive solar self-consumption to active flexibility participation. The context behind this shift is clear: residential storage installations in the Netherlands are growing rapidly, with around 166,800 battery systems expected by the end of 2025, the vast majority in households.

The Dutch grid is facing structural congestion, with more than 14,000 projects waiting for grid connections, pushing stakeholders to unlock flexibility from decentralized assets instead of relying solely on new infrastructure.

The results highlight how quickly flexibility models can scale. While residential storage alone is expected to reach around 1.3 GWh by the end of 2025, total battery capacity across all segments is forecast to grow to roughly 2.9 GWh, more than doubling year on year, with household systems contributing a significant share of new additions. This shows that decentralized assets, when aggregated and steered intelligently, have the potential to provide measurable grid relief while creating a viable business case for utilities. Another survey of 100 Dutch end users shows that 91% are already or are willing to actively participate in the energy market, a number which will likely increase as the end of net metering shifts cost signals toward active optimization.

Expert insights and future outlook

As Irene Guerra Gil argues, “The transition from ‘install and forget’ to active orchestration is the entry ticket to the next phase of the energy transition. By 2030, we expect the Dutch grid to be supported by a massive, decentralized network of home batteries and electric vehicles. For companies in this space, the value lies in providing the digital foundation that turns these assets into a reliable, flexible and profitable energy system.”

The Dutch energy landscape is shifting from isolated devices to connected layers, where software steers solar and battery behavior, storage supports system stability and flexibility scales without adding burden for installers or households.

What once ended at commissioning now continues through coordination, control and continuous optimization. And so too does the revenue opportunity continue and grow. The real shift is not bigger solar arrays or faster battery cycles, but a smarter operational layer that turns both assets into dependable system value.

FAQs: Getting started with solar and battery retrofitting in the Netherlands

Where should households start when considering solar plus battery after net metering?

Start with the existing setup, not new hardware. Many Dutch homes already have PV systems that can be optimized before adding capacity. Understanding current self-consumption levels, tariff structures and available flexibility programs helps determine whether a battery or smarter energy management delivers the biggest impact first.

Do solar and battery systems need to come from the same manufacturer?

No. Most retrofit projects in the Netherlands involve mixed hardware ecosystems. The key is ensuring devices can be coordinated through a manufacturer-agnostic energy management layer. Compatibility at the software level often matters more than brand alignment when scaling solar and battery systems.

What should installers prioritize when customers ask about adding storage?

Beyond sizing the battery (given their potential for flexibility use cases it makes sense to have a higher storage capacity than PV capacity), installers should assess how the system will be controlled after installation. As dynamic tariffs and flexibility markets expand, long-term value depends less on hardware capacity and more on whether solar and battery assets can be intelligently integrated and adapt to price signals automatically. A HEMS is the foundation of this. Check out gridX’s full compatibility list here.

How can OEMs differentiate in a crowded solar plus storage market?

Hardware alone is becoming harder to position as a unique selling point. OEMs increasingly differentiate through software capabilities, integration readiness and the ability to offer an energy management experience that connects solar, battery and other devices without locking customers into a single ecosystem.

What is the biggest mistake households make when shopping for solar and battery solutions?

Focusing only on upfront hardware costs. Long-term value comes from how well the system adapts over time – to policy changes, new tariffs and additional devices like EV chargers or heat pumps. Choosing solutions that support flexible control and future retrofitting often matters more than selecting the biggest battery on day one. gridX’s HEMS allows end users to reach a break-even on their asset investment up to five years earlier.