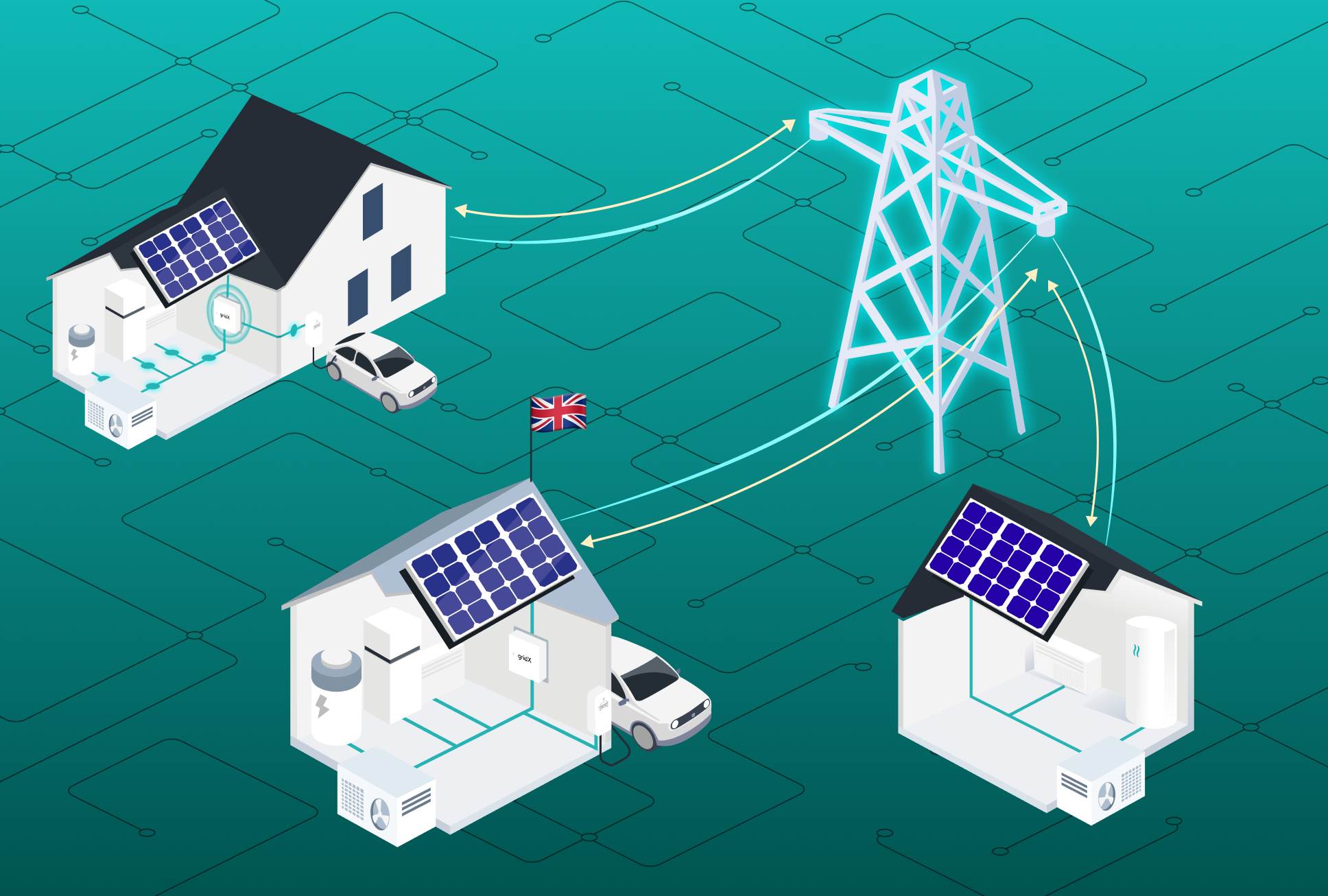

What is a home energy management system (HEMS)

A home energy management system acts as an energy manager and connects and controls a home’s energy devices through a central smart hub. It monitors real-time electricity use and generation, then intelligently adjusts devices to run more efficiently. For example, a HEMS can delay a heat pump or electric vehicle (EV) charger to off-peak times or prioritize solar energy usage when available. All this is typically managed via software dashboards or smartphone apps that give homeowners visibility and control over their energy flow.

Typical energy assets

- Photovoltaic (PV): A PV system, or rooftop solar, is often the first step to a HEMS as it allows households to become independent from the grid (and increasingly volatile electricity prices) and use locally-generated electricity to power the energy-consuming assets in their home. These usually include an inverter to convert the solar power into usable energy that powers household devices.

- Battery: A storage system can store surplus solar power when the sun is shining and allows it to be used later when it is needed.

- Heat pump: A heat pump is a highly efficient heating device powered by electricity that extracts heat from an external source rather than producing it. It can be powered by local PV and is therefore becoming an increasingly common part of HEMS.

- Electric vehicle (EV): EVs are another flexible energy-consuming asset. Because they usually sit for a long period of time, their charging can be shifted to periods when either solar generation is high or electricity prices are low. The car must be linked to the energy manager via a wallbox or other smart EV charger.

- Smart meter: A smart meter is an important element in a HEMS as it provides real-time information on household consumption.

- White goods: Household devices such as washing machines or fridges can also be controlled intelligently to optimize their electricity consumption.

Technical requirements

To implement a HEMS, there are certain technical requirements that must be met, to ensure seamless and consistent functioning of different distributed energy resources (DERs);

- A stable and reliable internet connection securing proper communication between the energy management system (EMS),server and each energy device would be beneficial but a local network would suffice

- A local gateway typically in the form of a central control unit, like our gridBox, that optimizes energy flows of multiple assets from numerous manufacturers on site. Cloud-based energy management is also possible without a local gateway, however, this is only suitable for the intelligent optimization of individual energy assets.

- Software and applications compatible with the hardware to control, monitor and access the DERs in a household.

- An energy tariff is integrated into the system - XENON is tariff-agnostic, meaning end users can remain with their current tariff provider or switch to a new one.

Use cases

Every household has its individual needs. Thus the use cases and applications may vary to fit specific demands. Home energy management systems can start with a basic setup involving a few assets and then become more complex to enable more savings.

- Monitoring: Gaining real-time data and visualization of the operational behavior, site-specific details and status of all connected assets.

- Self-sufficiency optimization: Maximizing the amount of self-generated power that is used to power the remaining assets in a home to minimize costs and emissions.

- Time-of-use (ToU) tariff optimization: Shifting the electricity consumption of connected DERs, such as heat pumps and electric vehicles, to times of low prices.

- Flexibility marketing: Monetizing the flexibility of assets by feeding energy back into the grid if there is excess power, for example stored in the battery, according to varying electricity prices and grid capacity.

- More advanced use cases: HEMS is the building block that enables larger-scale future energy use cases such as smart districts (energy is connected and optimized across a larger area), virtual power plants (the flexibility of multiple energy assets is aggregated and monetized by participating in wholesale markets) or energy communities (energy is shared via peer-to-peer trading).

Why HEMS are becoming essential

Europe’s energy landscape is changing rapidly. Soaring electricity prices and growing adoption of electric cars and heat pumps have pushed homeowners to seek smarter ways to manage consumption. A home energy management system helps households save money by using energy more efficiently and taking advantage of times when power is cheapest or most plentiful. It also helps reduce strain on the grid by smoothing out peaks in demand and feeding excess solar energy back when needed.

HEMS technology has advanced rapidly in recent years, becoming more interoperable, data-rich and easier to deploy. The parallel rise of smart home devices, volatile energy prices and policy incentives has accelerated HEMS adoption across Europe. Industry analysts project double-digit growth through the end of the decade, driven by the clear benefits: reduced energy bills, improved comfort through automation and greater control over energy use and emissions.

Equally important, an energy manager bring resilience and flexibility to the energy system. By coordinating solar systems, batteries and controllable energy-consuming appliances, a home can maintain critical functions during outages or high-price periods. According to energy experts, these systems serve a dual role: empowering consumers to manage their own energy while supporting the wider grid with valuable flexibility. In a decentralized renewable grid, houses with HEMS effectively become miniature power hubs that can respond to grid conditions – a cornerstone of intelligent energy solutions for the future.

HEMS in Europe: Market overview

Europe is at the forefront of home energy management adoption. By the end of 2024, an estimated 3.8 million HEMS were installed in European homes – a number that is growing fast. This still represents only about 3% of households, but that share is projected to nearly triple to 8.5% by 2029. Europe’s push for renewables and energy efficiency is a big driver behind this trend. Governments have introduced incentives for residential solar, home batteries and smart energy tech to support climate targets. Moreover, recent volatility in energy prices and even regional blackouts have underscored the value of energy autonomy at home, boosting interest in HEMS.

Germany is by far the largest HEMS market in Europe, accounting for nearly half of all systems installed. But other Western European countries are catching up quickly, especially the UK and the Netherlands which are investing in smart grids and home renewables. Each country’s approach to home energy management is shaped by its unique policies and infrastructure. Below, we dive into how the UK, Germany and the Netherlands are each fostering HEMS adoption.

Germany: Self-consumption, solar optimization and new regulations

Germany’s home energy management approach is shaped by its mature solar market and tightening regulations. With approximately 70–78 GW of rooftop PV capacity installed across homes and small buildings – most of it without batteries or EMS – there is significant untapped EMS retrofitting. These legacy systems lack the ability to store excess energy, shift loads or respond to tariffs or grid conditions, making self-consumption optimization the clear priority for next-phase upgrades.

Historically, Germany’s smart meter rollout was delayed, holding back dynamic tariffs and demand response. That’s changing: new laws now mandate smart meters for systems >7 kW and flexible tariffs from 2025. Regulations like §9 EEG impose a 60% export cap until smart meters are installed, while §14a EnWG requires controllability of high-power devices like EV chargers in exchange for lower grid fees – up to €750 savings per year. A smart energy manager handles these requirements automatically, ensuring compliance while optimizing performance.

HEMS adoption is also driven by §14c EnWG, which enables DSOs to send dynamic consumption or export limits, and §19 EEG, which opens the door to market-based operation for small PV+storage systems. These changes push homes toward active participation in grid services and direct power marketing.

Despite past policy gaps, German homeowners have responded to energy cost pressures with rapid uptake of clean energy systems. It’s now common to see solar, storage, heat pumps and EV charging in homes. Increasingly, homeowners are adding HEMS to cut bills and improve energy autonomy. Subsidies and local rebates support this transition. Retrofitting is becoming a more important trend that allows energy players to tap into the millions of homes that have already installed energy assets: making them smart and adding new assets empowers these homes to enhance both savings and grid stability. As smart infrastructure scales, Germany’s HEMS are shifting from simple self-consumption tools into critical, flexible grid assets.

Netherlands: From net metering to smart flexibility

The Netherlands’ HEMS journey is evolving as the country shifts from lucrative net metering toward a smarter, flexibility-based energy model. For years, Dutch households benefited from the net metering (salderingsregeling) scheme, allowing them to offset exported solar power at the same rate as grid imports. This drove widespread rooftop PV adoption – one of the highest per capita rates in Europe. But the government has confirmed a phase-out: net metering will start to taper in 2027 and disappear entirely by 2031. At the same time, grid congestion is increasing, and electric heat pumps and EV chargers are becoming standard. These shifts make it clear: self-consumption and grid-responsive behavior will define the next phase of value creation.

Most Dutch households are already technically prepared. Over 90% have smart meters, enabling automation, dynamic tariffs and participation in emerging flexibility markets. Grid operators, through Netbeheer Nederland, are redesigning tariff structures to encourage off-peak use. Platforms like GOPACS (a non-profit joint initiative of all Dutch grid operators) allow aggregators to trade localized flexibility, and the Dutch government is supporting “smart steering” of EV chargers and heat pumps to help balance the system. A national Smart Charging Action Plan aims for 60% of EV charging sessions to be time-optimized by 2025, and similar incentives are encouraging demand shifting with heat pumps.

This environment aligns directly with gridX’s flexibility use case: imbalance optimization in the Netherlands. By aggregating the flexibility of distributed residential assets – like batteries, EV chargers and heat pumps – energy providers can support system balance and generate additional revenue. Homes participating in gridX-enabled flexibility programs can earn up to €6 per day per system, simply by making flexibility available on the Dutch imbalance market. With grid volatility increasing, this kind of orchestrated load balancing turns passive homes into active contributors to grid stability and revenue streams.

For now, net metering remains in place, so many solar-equipped homes still delay adopting storage. But that window is closing. As the salderingsregeling regime winds down, dynamic export pricing will expose consumers to real-time market signals. In response, residential storage and HEMS adoption is expected to rise sharply before 2027. Battery vendors already report a surge in demand from homeowners looking to protect solar ROI, and energy management platforms are quickly becoming the standard for managing load, storage and pricing signals in tandem.

The Dutch energy landscape is shifting from a subsidy-driven solar model to an integrated flexibility ecosystem. HEMS are central to this evolution. They not only optimize solar self-use and cost savings but now offer real market participation – turning smart homes into grid assets. As policy, technology and business models converge, the Netherlands is emerging as a leading testbed for decentralized, responsive energy management at scale.

United Kingdom: Smart meters and dynamic tariffs drive adoption

The UK’s strategy centers on widespread smart meter deployment and dynamic electricity tariffs. A national rollout, aiming to cover most homes by the mid-2020s, has already equipped over 50% of households with smart meters. This foundation enables utilities to offer time-of-use pricing that rewards shifting demand to off-peak hours. Some suppliers now provide EV charging tariffs or overnight rates well below daytime prices. These flexible tariffs are only possible thanks to half-hourly usage data from smart meters.

Policy support has also accelerated home energy upgrades. Since 2022, VAT on solar panels, batteries and other energy-saving tech was removed, lowering costs. While feed-in tariffs ended in 2019, the Smart Export Guarantee offers modest compensation for exported solar, pushing self-consumption to the forefront. The 2022–2023 energy crisis, with prices exceeding £0.30/kWh, highlighted the value of producing and storing one’s own energy. Battery adoption surged – over 22,000 systems were installed in 2024, quadruple the year before. The government also piloted a national Demand Flexibility Service that paid households to reduce peak demand, proving how smart homes can stabilize the grid.

The UK’s transition challenge now is integration. Roughly 3.2 million homes already have at least one electrified asset – PV, EV charger or heat pump – but most operate in silos. Of the ~7 GW of residential PV, the majority lacks storage or EMS integration, leading to uncontrolled exports. Nearly 300,000 wallboxes and 450,000 heat pumps are in use, yet few are linked to household control platforms. In addition, these assets must become G100-compliant, meaning they operate in a grid-friendly manner. This makes the UK a retrofit-first market, where real value lies in connecting these systems with automated, regulatory-compliant energy management. By upgrading existing assets, households can cut costs, enhance flexibility and support grid stability.

Policy comparisons and incentives

National policies have a profound influence on how HEMS are adopted across these countries. Here’s a quick comparison of the policy landscapes in the UK, Germany and the Netherlands and how they drive (or hinder) home energy management:

Smart metering

The Netherlands leads with near-universal smart meter coverage. The UK is quickly catching up (about 60% in 2025) with a mandated rollout ongoing. Germany lagged far behind but is accelerating deployment through recent legislation. More smart meters mean more opportunities for dynamic pricing and HEMS optimization in a country.

Solar export incentives

Germany and the UK both moved away from generous solar buyback programs. Germany’s feed-in tariff for new systems has been slashed to minimal levels (around €0.06/kWh) , and the UK’s former feed-in tariff was replaced by the lower Smart Export Guarantee. Both thus strongly incentivize using solar energy on-site with HEMS rather than exporting. The Netherlands until now had full net metering (1:1 credit) which dis-incentivized HEMS, but its abolition by 2027 will align Dutch policy with the others.

Dynamic tariffs and demand response

All three countries are exploring or implementing time-varying electricity prices. The UK has competitive retail offers for smart time-of-use plans and even pays consumers to cut usage at peak times. The Netherlands has enabled dynamic tariffs (thanks to smart meters) and some providers have introduced them, though uptake was low under net metering. Germany historically had almost no residential time-of-use tariffs due to meter delays, but as digital meters roll out, new dynamic and peak load pricing schemes are expected.

Electric vehicle and heat pump integration

The policy push for EVs and electric heating is common to all three. The UK and Netherlands in particular have aggressive EV adoption and phase-out of gas heating, which increases residential electricity demand. Governments are encouraging “smart charging” standards (the UK now requires new home EV chargers to be smart-capable) and incentives for load shifting. Germany’s grid codes (e.g. EnWG §14a) allow utilities to manage EV charger and heat pump loads during grid stress, implying the need for smart control systems in homes. In essence, HEMS functionality is becoming part of the regulatory expectation for managing new electric loads in all these countries.

While each nation’s approach differs, the overall trend is convergence toward a future where homes are not passive energy users but active participants in energy markets. Supportive policies – from funding battery subsidies to updating grid rules – are emerging to ensure HEMS and other intelligent energy solutions flourish across Western Europe.

Expert insights: The future of HEMS in Europe

Industry experts agree that home energy management is fast becoming a cornerstone of the modern energy system. As Nikolas Fröhle, HEMS Product Lead at gridX, emphasizes, resilience and smart automation at the household level are no longer optional:

“A well-designed energy manager brings clarity to complexity. It helps households lower costs and increase independence while giving energy providers the flexibility they need. At gridX, we build systems that work seamlessly for both sides. Smart at the edge. Stable at scale.”

This insight underlines a key point – HEMS technology is more than just about convenience or savings, it is about building a robust, flexible energy ecosystem from the ground up. By equipping homes with intelligent control and connectivity, we empower homeowners to weather price spikes or blackouts and contribute grid support services behind the scenes. The expert view is that Western Europe’s early investments in HEMS will pay dividends in energy security and efficiency. Energy professionals and utilities should note that these systems are evolving from nice-to-have gadgets into strategic assets. In the words of one gridX report, what was once a niche add-on is now “the new standard for resilience” in an increasingly distributed grid.

Western Europe’s embrace of home energy management systems reflects both how technology is enabling smarter energy use and why it is critical for a sustainable future. Germany, the Netherlands and the UK illustrate that while policy paths vary, the destination is the same – empowering consumers with intelligent energy solutions that benefit both the household and the wider power network. Homes outfitted with HEMS are more efficient, more autonomous and better equipped to handle the energy challenges of the coming decades.